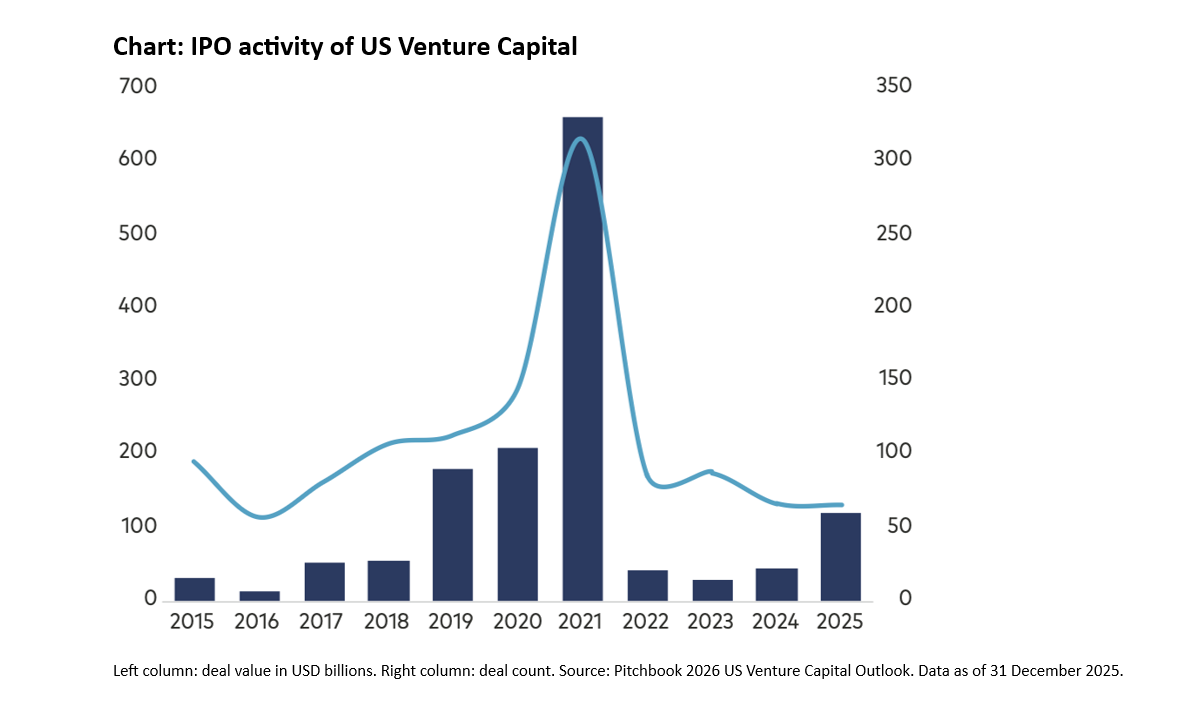

Venture capital: Access to the next generation of market leadersBY THOMAS KRISTENSEN | WEDNESDAY, 10 JUN 2026 4:01PM As companies stay private for longer, a growing share of value creation takes place before investors can access them through listed markets. Investors who rely mainly on listed equities may therefore enter important innovation cycles only after much of the upside has already been realised. Venture capital can help close this gap - but access, manager selection and disciplined portfolio construction are decisive. Venture capital has long occupied an ambiguous place in portfolios. It attracts attention through unicorns and stories of exponential growth, yet is often treated as peripheral because outcomes are volatile, dispersion is extreme and cash flows are slow. This view is increasingly misaligned with how value is created in the modern economy. Over the past two decades, value has often been generated earlier in the lifecycle of a company and increasingly in private markets. Investors who only hold public equities and buyouts may therefore be structurally late to important innovation cycles. A strategic building block This has important implications for portfolio construction. Venture capital should not be regarded simply as "high-risk equity". Instead, it can be viewed as a strategic building block because it increases diversification, helps hedge disruption risk and provides access to increasingly institutionalised manager capabilities. The diversification effect is broader than it first appears. Venture provides exposure to earlier-stage innovative companies - an investable segment that has become structurally less accessible through other channels. Public markets no longer represent the full corporate lifecycle, as many of the most consequential companies remain private for much longer. Venture therefore provides exposure to a different slice of capital investment that traditional public equity and buyout portfolios increasingly struggle to capture. Venture capital also addresses a risk often hidden in traditional portfolios: disruption. Innovation accelerates in waves, from electrification and automobiles to the internet, mobile computing, the cloud and artificial intelligence. During such super-cycles, established companies can come under pressure quickly. Public indices, by construction, are often weighted towards past winners, leaving many portfolios with concentrated exposure to incumbents. Venture can help address this imbalance by giving investors exposure to the challengers driving disruption. At the same time, the venture ecosystem has become more institutionalised. Historical criticisms relating to illiquidity, opacity, manager quality/performance dispersion and the perception that it embodies "art over science" are real. However, the ecosystem has evolved materially over time, with more larger platforms emerging, specialized managers addressing more recent investment themes, deeper secondary markets, better data and a broader set of access routes for institutional investors. When exits take longer, liquidity becomes key The path to liquidity has always been central to venture capital's value proposition. For decades, companies matured in private markets before exiting through IPOs or acquisitions. Today, investors no longer need to rely solely on market-driven events to get liquidity. The evolution of the secondary market in venture capital allows for engineered, negotiated and permissioned processes to generate liquidity before an eventual IPO. As traditional exits have faded, secondary markets have become a cornerstone of venture liquidity. For investors with the right access and underwriting capabilities, this can create attractive opportunities. Secondary investors can buy stakes after key technical and product risks have been mitigated, use real operating data to underwrite investments and acquire positions at discounts driven by liquidity needs rather than fundamental weakness. Why scale matters This leads to a central issue in venture capital: platform scale. Venture capital is not an asset class where generic exposure is likely to be enough. Outcomes depend heavily on the managers and companies that an investor can access. Scale can therefore make a material difference. Larger platforms can build relationships across vintages, geographies and stages, improve allocation to oversubscribed opportunities and reduce informational disadvantages through broader market visibility and benchmarking. As venture portfolios grow more complex, scaled platforms can also participate across primary funds, secondaries, co-investments and direct opportunities. In this sense, scale is not about size for its own sake; it is about proximity to information, relationships and the outlier outcomes that drive returns. Venture capital remains demanding: outcomes are skewed, underwriting is difficult, patience is required and access is limited. But the economic map has changed. For sophisticated investors, venture can potentially offer exposures that are difficult to replicate elsewhere.

|

Latest News

MST Financial broadens services to Alder & Partners

Australia welcomes 25k to millionaires' club: UBS

Family office succession takes back seat to investments

Lowy family takes stake in Magellan

Cover Story

Generation next

FINANCE DIRECTOR

GOWING BROS LTD

Expert Feed

What I told a room of financial advisers about divorce

It's a commodities supercycle, but not as you know it

How your clients can start leaving a legacy now